How Do I Buy a New Home Before Selling My Current One in 2026?

How Do I Buy a New Home and Sell My Current One at the Same Time?

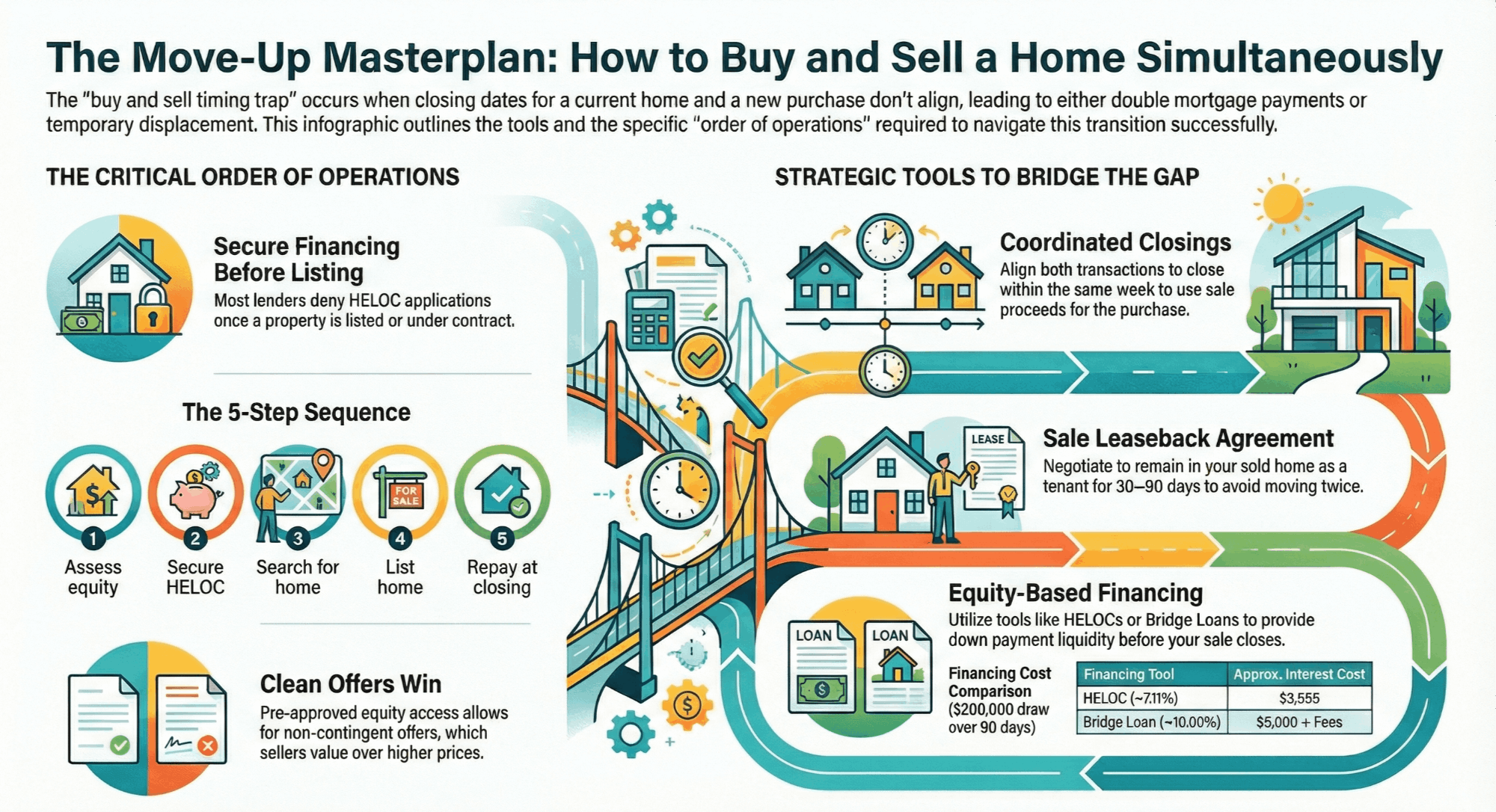

Quick answer: You have three primary tools. You can align closing dates, negotiate a sale leaseback so you remain in your home temporarily after selling, or secure equity based financing before you list. Most successful move up homeowners use more than one of these strategies together.

If you are preparing to move, you are facing one of the most common coordination challenges in real estate. The risk is owning two homes at once or having no home between closings.

This guide explains your realistic options, the financial math behind each one, and the correct order of operations.

What Is the Buy and Sell Timing Trap, and Why Does It Happen?

The buy and sell timing trap occurs when the closing date of your current home does not align with the closing date of your new purchase. This creates a temporary financial or housing gap.

Each transaction involves independent buyers, sellers, lenders, inspectors, appraisers, and attorneys operating on separate timelines. Even well managed deals can slip. The result is a gap measured in days or weeks.

There are two primary outcomes.

The first is owning two homes. You close on your purchase before your sale completes. You carry two mortgage payments, two tax bills, two insurance policies, and duplicate utilities and maintenance costs.

The other is temporary displacement. You close on your sale before your purchase is ready. You move into short term housing while your belongings go into storage.

Neither outcome is catastrophic. Both require preparation.

How Can I Avoid Owning Two Homes at the Same Time?

The most reliable method is coordinating both closings within the same week, ideally the same day. Sale proceeds from the first closing fund the second.

Back to back closings are common in active markets. When timelines hold, the transition is seamless. If underwriting or appraisal delays occur, a backup strategy becomes necessary.

Successful coordination requires:

- Agreement on a target closing date during contract negotiation

- All contingencies cleared early

- Clear to close confirmation from the lender several business days before closing

- Consistent communication between agents, attorneys and lenders

You cannot control your buyer’s underwriting timeline. A delay on the sale side can create the need for interim financing.

What Is a Sale Leaseback Agreement and How Does It Work?

A sale leaseback allows you to sell your home and remain as a tenant for a defined period, typically 30 to 90 days. This gives you time to close on your purchase without moving twice.

The arrangement is negotiated in the purchase contract. You pay the buyer a daily rent beginning on the day of closing.

Important terms include:

- Daily rental rate, often based on the buyer’s principal, interest, taxes, and insurance divided by 30

- Maximum leaseback duration

- Security deposit handling

- Responsibility for property condition during occupancy (which usually includes a minimum 5% of the purchase price held in escrow until the seller vacates the property)

If the buyer is financing the purchase, their lender may limit leasebacks to under 60 days for primary residence qualification under Fannie Mae or Freddie Mac guidelines. Confirm this before signing.

What Financing Options Can Bridge the Gap Between Buying and Selling?

Three tools typically bridge the gap: bridge loans, HELOCs, and home equity loans.

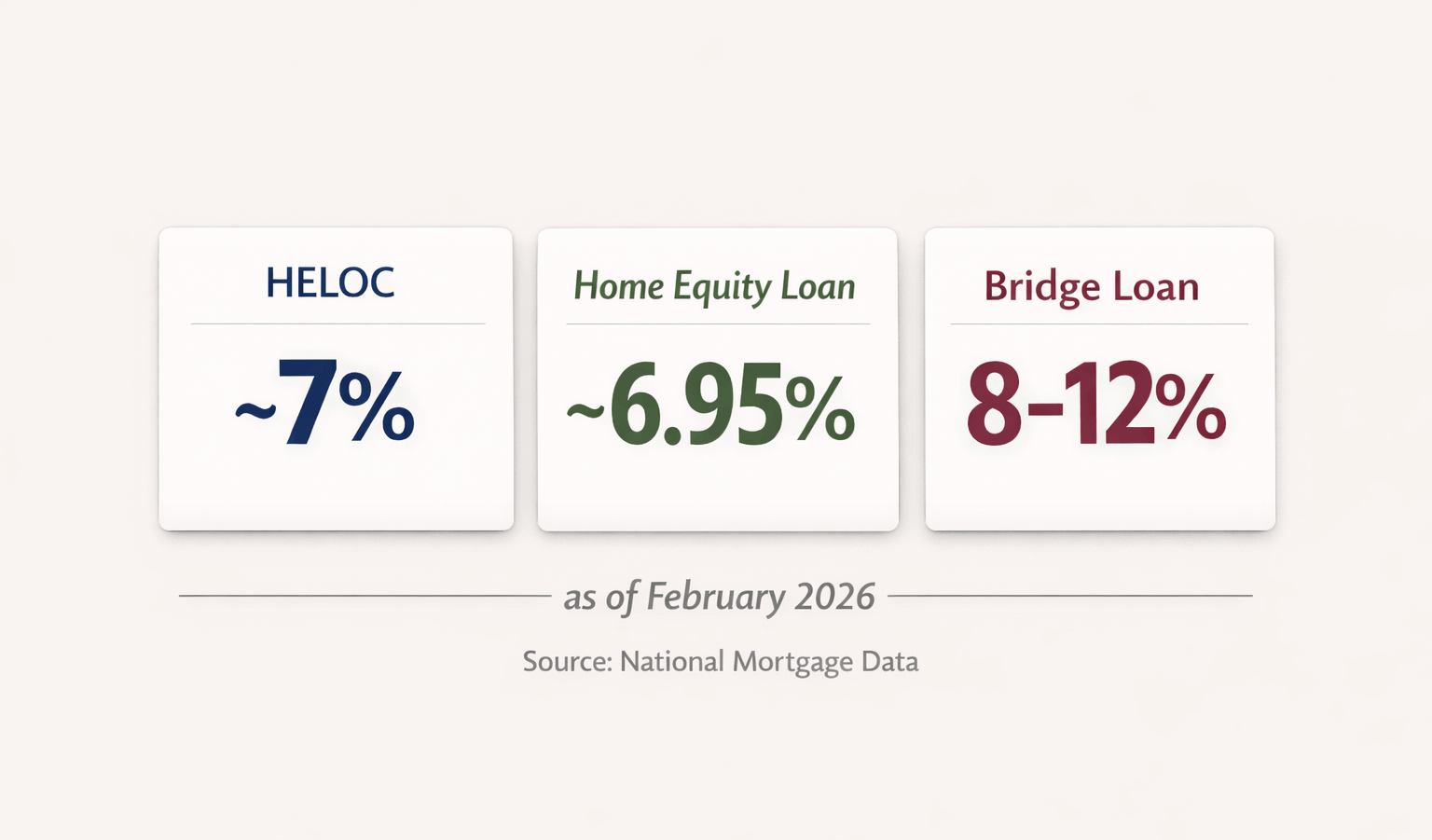

Bridge loans are short term loans, usually six to twelve months, secured by your current home’s equity. Rates commonly range from approximately 8 percent to 12 percent, with origination fees between 1 percent and 3 percent. They are designed specifically for transitional financing and can close quickly, but they are more expensive.

A HELOC, or home equity line of credit, is a revolving credit line secured by your home’s equity. As of late February, 2026, the national average HELOC rate is approximately 7% according to the cited data. HELOCs typically allow interest only payments during the draw period and charge interest only on the amount borrowed.

A home equity loan is a fixed rate lump sum loan secured by your home’s equity. As of February 20, 2026, the national average home equity loan rate is approximately 6.95 percent. This option provides predictable payments during the gap period.

Both HELOCs and home equity loans are generally lower cost than bridge loans, assuming qualification.

Why Must a HELOC or Home Equity Loan Be Secured Before Listing?

Most lenders require the property securing a HELOC or home equity loan to be owner occupied and not under contract during underwriting. Once the property is listed or under contract, many lenders will deny the application.

This timing requirement is critical.

The recommended order of operations:

- Assess your equity and market value

- Apply for and secure the HELOC or home equity loan

- Begin searching and negotiating on your next home

- List your current home with coordinated timing

- Repay the equity line or loan at closing

How Much Equity Is Required?

Most lenders allow a combined loan to value ratio of approximately 80% to 85%. Available borrowing equals appraised value multiplied by allowed CLTV, minus your current mortgage balance.

Additional qualifying factors include credit score, often 620 to 720 or higher, debt to income limits, and verifiable income.

What Is the Cost Difference Between a HELOC and a Bridge Loan?

On a $200,000 draw for 90 days, a HELOC at approximately 7% results in about $3,450 in interest. A bridge loan at 10% results in roughly $5,000 in interest for the same period, plus origination fees that may range from $2,000 to $6,000 depending on lender and structure.

The difference can exceed several thousand dollars, depending on loan size and duration. Actual costs vary by credit profile and lender.

What If I Cannot Qualify for Equity Based Financing?

If you cannot secure a HELOC or home equity loan, the remaining options include:

- Bridge loan financing

- Contingent purchase offers

- Selling first and renting short term

- Negotiating extended closing timelines

Each option involves tradeoffs between cost, flexibility, and risk tolerance.

How Does the North Shore Market Affect Timing?

In supply constrained segments, well priced homes tend to sell efficiently. This can create scenarios where a homeowner identifies their next home before their current home is listed.

Pre-approved equity access provides flexibility and allows for stronger offers. In competitive situations, clean offers without sale contingencies often outperform contingent offers, even at higher prices, because sellers value certainty.

Frequently Asked Questions

Can HELOC funds be used for a down payment?

Yes. HELOC proceeds may be used for a down payment. Your mortgage lender will include the HELOC obligation in your debt to income calculation.

What happens to the HELOC when my home sells?

The HELOC balance must be repaid at closing from sale proceeds, similar to your primary mortgage. The line then closes.

How long does HELOC approval take?

Typically two to six weeks, depending on lender and appraisal requirements.

Can my home be under contract and still qualify?

Most lenders will not approve a HELOC on a property that is listed or under contract.

What is the difference between a home equity loan and a cash out refinance?

A home equity loan adds a second loan while preserving your existing mortgage rate. A cash out refinance replaces your first mortgage with a new loan at current rates.

Do I need to sell before getting pre-approved for a new mortgage?

No. However, lenders include both mortgage obligations in debt to income calculations, which may affect approval limits.

Is sale leaseback rent taxable income to me?

No. You are paying rent to the buyer. Standard capital gains rules apply to the property sale.

What are my costs if I temporarily own two homes?

You would carry both mortgage payments, property taxes, insurance, and utilities. Budget planning should account for this possibility before making a move up offer.

Ready to Plan Your Move?

Effective coordination begins with strategy and sequencing. Review your equity position, financing options, and timing before entering the market.

Categories

Recent Posts